From May to June, the biggest mover in the portfolio would be Huationg Global. The rest of the stock had relatively lesser movements in terms of %.

On the results / business updates front, there is nothing much to report as there is no results release in June.

YTD, the STI Index is down around 1.39% and in June it is up around 1.49%. Just relieved that the results this year has been much more pleasing compared to the poor results seen in 2022 where i clocked a -16.56% performance.

July and August should see more volatility ahead as results release is upcoming and speculating of results might occur as well.

The past few months have seen some changes in my portfolio. Will just jot down the changes and the reasons (shortened version) for the changes.

Should i be able to find some time i will consider writing a longer version of certain changes

(1 of the associates of my recent additions)

Removals

Ossia Intl - Following a result that has met expectations, the share price has increased by over 20% from the results release. As i have only initiated positions since March my average price is around 0.12x.

Stripping aside the presidential bid craze and all, the dividend yield of 10.5% and PE of 4.3 is attractive. However considering Harvey Norman has a PE of 5.3, expected retail environment to be tough as well as my intention to channel limited funds to something else, i have decided to divest it and review the company 3 months later.

It is fair to say that the estimation was on the lower end of my expectations as well.

AAG Energy - With the offer at 1.85 approved, i have divested on the last day of trading at 1.83 as the 1+ months wait would be too long for myself as i have decided to take a risk and try to use the funds to do channel to something else.

Central China Management - I only have less than 2% of my networth in this stock but i have decided to clear the deadweight anyway. This brings an end to any involvement i have with central china stocks for the time being. As such i can keep lesser eyes on the property market and more on other stocks in my portfolio. The final divestment was done in May at a price of 0.415. Price as of 27 June is 0.335 so guess i am right in the short run for now.

Additions

When in doubt, just add things in your portfolio. Yup that is what i did so the usual suspects have seen an increase in their positions. However, there is one new addition to the list.

Yeebo International (Hkex: 284) - A company that has its own business that has shown improvement in bottomline in the past years. Financially healthy and way below book value as the associates it holds has far outweigh the market value.

Being associates, they contribute to the company's bottom line as well which has improved over the years.

As a whole, it is trading at 0.3 to its book value. With some divestments done in 2022 to its associates, it remains to be seen if the same will happen in 2023 but since its associates are recording better profits, it will benefit slowly as well if it chooses not to sell the golden goose to the market.

I have took up a stake following proceeds of AAG Energy. I foresee adding more when the company divest more of its associates shareholding or when the associates report better results and have a good roadmap being executed. But for now, buy some and observe and if by luck anything delightful pops up then its all good.

Dream International, Mainland Holdings and Huationg Global which has already been in my portfolio are the other additions. To sum each addition in 5 and less points each.......

Dream International

-Weak US Orders Expected due to Funko Q1 Earnings Poor and Full Year Expected to be Weak.

-Betting on the increased orders from Disney Japan and China.

-Increased expansion and hiring through Covid shows faith in business

-Good Dividends, best financial health in years and below book value

-IR replied, while quality of answer might not be the best but it will suffice.

Mainland Holdings

-New Factory came into production in May, will observe how the production and margins improve

-Guided double digit growth for 2023 in Dec 2022. To see if this plays out

-Factory in Bangladesh being lauded for success of OBOR and Common Prosperity

-Reputable Management, Hosting of Key Customers to new factor in May .

-Hiring of Jap Language Knowledge Staff might indicate new customer / market as jap revenue is low now.

Huationg Global

-High Risk Stock, Financial Statements and Audited Reports actually look difference with huge disparity.

-Red Flag of CFO Leaving adds to the high risk. Although removing a CFO that prepares statements with disparity from audited reports does make some sense

-Inland Logistics Support related to construction activity showing strength. With projects lasting 1 year, can we expect results to sustain this year? Hopefully.

-Possible Divestment of Office might be catalyst as in the audited report, the sale value > book value.

-Dormitory revenue low compared to peers. Might see a catch-up or higher amount this year due to demand supply factors?

The computer is back up so i will celebrate by posting a post.

As the title goes, today's stock focus will be on Honma Golf (Hkex: 6858)

Honma Golf is considered to be a small player in the golf industry and a premium brand by many. A video of their golf club making can be found on youtube.

Layman Technical Analysis

Looking at the 5 years price chart, the stock has came down close to 66%. Looking at the current price, it seems to be trading at close to 5 year lows.

Financials

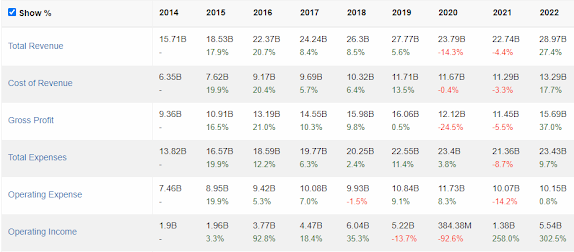

Looking at its revenue and income trends, it does not have a stable trend and it has been affected during 2020 and 2021 as well. What is worth noting is that it has made a good recovery in 2022 to pre-covid levels.

As of 2022 FY, its operating earnings is around 0.4 HKD, this translates to a pe of around 8.3 at current price of 3.32.

Reasons to consider this stock

1) Growth in revenue of golf club. 1 of its most important source of revenue, golf clubs have seen a growth in revenue under constant currency basis. Traditionally, 1H has been lower in revenue so there is a good chance that if the momentum continues, the company could see record earnings in this FY.

Mizuno's golf department recorded an increase of around 30% from April 2022 to March 2023. As such, i believe that Honma has some chance of doing well as well.

2) Golf as a sport. In the past i have the idea that golf is for the rich due to the need to book a golf course, hire caddies etc. But as technology and more mainstream golf has been introduced, folks can now play golf at simulators first as well as tee-up at driving ranges before going onto playing golf course golfs. As such, the market has opened up with the use of technology. These simulators are also available as 'club try outs' as players can now tee up at the stimulators to see if the golf clubs are suitable for them before purchasing it.

I believe the introduction of technology in Golf will allow Honma to have higher brand awareness as folks can try their club before deciding to buy it, Honma being an expensive brand would deter others to purchase and try it in the past without such simulators.

3) Small Market Share Compared to Industry.

In 2022, the golf club revenue came in at around 200 million SGD. This is similar to Mizuho (244 million SGD) but small compared to others like Callaway (1777 million SGD) and Titleist (748 million SGD)

As such, it is less likely to be affected by any headwinds and more of the revenue will be focused on its execution.

Lastly, the internal target / guidance given at the recent half year result release will be 10+% target in growth in revenue while keeping net profit at 25% Margin.

Reasons to not consider this stock

1) Choppy Earnings - As the yen has been depreciating against many currencies, this has resulted in net profit to be very volatile. As such, it is more important to consider the operating profit instead. Should yen continue to depreciate further, the company would be worth lesser as well as its balance sheet since it is traded in HKD.

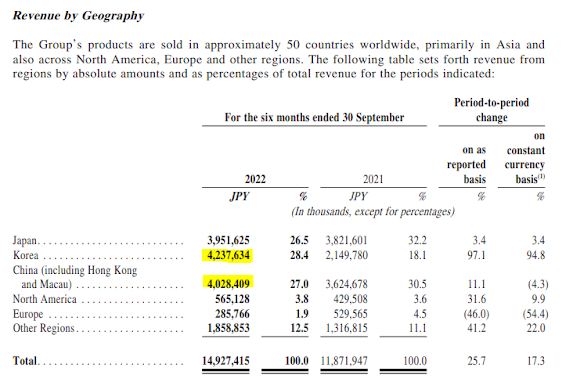

2) China and Korea are the biggest markets.

This can be seen in 2 ways. Firstly, golf in Korea and China are both fast growing and under penetrated.

However, i think it might be a concern as China has seen soft consumption since 2023 while Korea's rapid growth might not be repeated and even see declines. Golfzon, a indoor golf simulator provider has seen a revenue decrease of close to 20%. Similarly, a post by Invest Chosun has mentioned about the headwinds in the golf market in Korea in 2023.

Nevertheless, these are operating difficulties that the company has to navigate through.

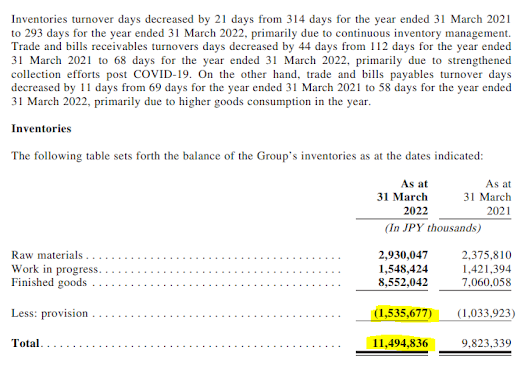

3) Inventory a Big Problem

Inventory is around 6 months of Revenue. Provisions have also increased by 50% across a span of 1 year.

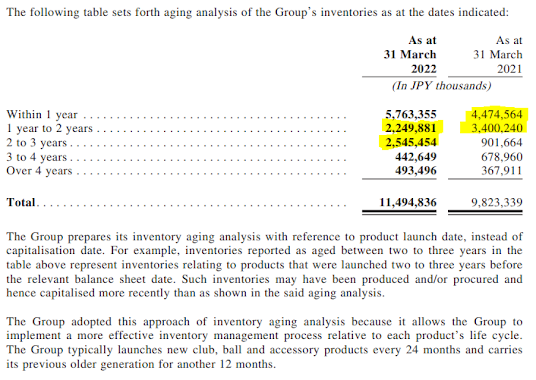

The company also does not have a good record in clearing inventory.

2.2 million out of 4.4 million fresh inventory was cleared in the first year resulting in 2.2 mil brought over.

Out of 3.4 million (1-2 years) inventory, only 855k inventory was cleared resulting in 2.5 million brought over.

As such, there is a probability on increased provisions.

Conclusion

Premium Brand, Healthy Balance Sheet but revenue and inventory remains a concern that the company has to overcome. The fall in share price to a single digit PE is probably justified given the concerns of the company.

Given that peers like Callaway and Acushnet trade at 15 to 25 PE, Honma is definitely undervalued at 8.3 PE.

Unfortunately given the current landscape and how other golfing peers have performed from Oct 2022 to March 2023, i believe the 2H growth might be cap at 10-15% max.

Having said that, the company is still small and has ample abilities to make up for the macro headwinds. If the share price is anything to show for, it shows that the company has depressed investors more often than not.