February 2022 Returns: 1.33%

Year to Date Returns: -6.29%

Since Inception (9 Sept 2020) Returns: 59.72%

As most companies on the list have reported results. It is a busy month with a flurry of results. I had a glance at most results so i would just give a short commentary. With the current uncertainty in the market, i think that the portfolio's result has reflected some of the sentiments and the other portion is slowly adjusting to the results release.

1) UMS - 4Q Profit before Tax is good, with a higher dividend. However the current investing sentiment and environment is not beneficial for tech related stocks.

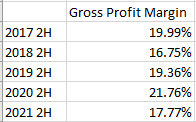

2) Propnex- Relatively weaker quarter on average compared with the full year. However the current PE is around 11 and the projection is slightly weaker transaction volume by Propnex. As such, being able to expand its sales force and capture more market share will be crucial in its growth.

With resale housing and condo off to a increasing price trend in 2022 despite lower volume in resale condo, it is estimated that a modest increase in housing price is expected but we have to consider inflation rate increase as well as general increase in interest rates which might play. I believe results for the year should come in at a range of -30% to +5% of 2021 results. Nothing too surprising but its not particularly a big shock. With regards to the position i will consider in the following month on whether to switch it out or not.

3) Q&M Dental - Results a minor shock, Acumen Diagnostics still the gem moving forward. With the ability to test and come out with test kits, the company is in a good position although it might see reduced impact due to the reduction in pcr testing and the increase in ART testing.

The 4th quarter result definitely tanked as more money has been spent on employee expense and it is a significantly higher % of the revenue in 4Q than the full year.

I think allowing another 3-6 months to see how acumen diagnostics do will still be acceptable.

4) TC Auto - Results looked ok to me. I was not expecting much from it apart from a result that is similar to 2020. As such, with the supply chain issues and china consumerism weakening sentiments, the company has managed to sell more automobiles in 2021.

A bright spot is its pre-owned cars and fleet sales commissions which has seen a growth in 2H 2021 compared to 1H 2021.

5) Hanwell - The consumer business recorded a slight decrease in profit. Tat Seng analysis has been written in previous post. This position will also be reviewed in the upcoming months

6) Centurion - Results look good but i need to read deeper to analyze it more.

7) Tuan Sing - The listing of GulTech should still be the main thesis. Currently trades at 0.41 book value.

8) China Sunsine - I think the results are good actually. Of course it is a cyclical industry and it is a china stock hence the current PE being less than 10 is understandable.

9) Straco - Results of aquarium acceptable. Singapore flyer continues to depress and the close down in January is likely to continue its depression (unsure if there will be any insurance claim again)

Perhaps an interesting thing would be the company making 2.5 million profit from finance income net of finance expenses.

10) Uni-Asia - Dividends can be better. Results is a beat as the net profit of 18 million is a beat against estimates of KGI (12.4 million) and UOB KH (17.1 million)

Need to analyze a bit deeper for the various business segments.