On a more serious note, a couple of companies released their earnings or guidance.

iFast - In what is a depressed market conditions from April to June, it is not a surprise that earnings came in at a depressed level even if the impairment is not accounted for.

China Sunsine - Released a positive profit guidance on 29 July after trading hours, will be interesting to see how it trades next week although i don't think it will have a huge effect since there is the S-Chip Risk as always.

Trans China - Released a negative profit guidance stating that profit will be lower than 1H 2021. Can't say i am surprised since there is so many mini lockdowns in China in 1H 2022 and some peers such as Pang Da Automobile (SHA: 601258) recording losses in 1H 2022 while BetterLife Holdings Limited recording 35% drop in profit for 1H 2022.

The thesis remains the same, trades at a valuation that is cheaper than peers, demand for cars will come back, its not china property where you pay and you only get half the car or a car without 2 wheels. Besides showing off a car is much better than buying properties these days.

Now back to the questions to ask when i review the portfolio.

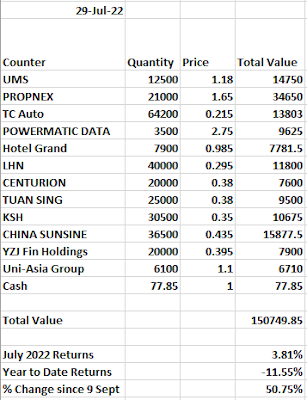

1) Is it time for Hotel Grand to make its grand appearance?

I have thought about it long hard and deep. I have decided to add Hotel Grand into the portfolio. This is on the back of an encouraging tourism numbers i have seen from Australia, New Zealand and Singapore.

Australia has the most amount of rooms for Hotel Grand, followed by Singapore then New Zealand.

Australia Tourism is up 730% in 2022 1st 5 Months compared to 2021 1st 5 Months

New Zealand is up close to 59% in 2022 1st 5 months compared to 2021 1st 5 Months.

Singapore Tourism Arrivals is up 1167% in 2022 1H compared to 2021 1H. With Revpar up 89% yoy and Occupancy Rates up 17.3% yoy.

All in all, with the privatization offer of Frasers H Trust at Close to Book Value, Hotel Grand looks like a steal with its low gearing and turning macro environment. Of course there is Covid and all but i have seen people around me starting to travel and to places including Australia, NZ as well.

I think we might be close to the stage where everyone just walks around with symptoms of Covid having caught Covid and only testing if travelling requires it or they need to see the doctor.

A slight concern would be the strengthening of SGD against NZD.

2) Am I adding any materials / commodities and inflation riders ?

In SGX, we are quite restrictive in choices. Oil intermediaries are not exactly best hedgers. Coal companies have had a weird run up and down then slightly up again. As for the oil producers, they are not exactly well known names that have been consistently pumping for many years like companies listed elsewhere. As for shipping i have mentioned previously so do check my previous posts.

There is some interest in adding some cement stocks etc such as Pan United but its valuations does not match my buy thoughts. Engro Corporation is another cement play but it has other businesses that makes it too complicated to break it down at times.

I feel that TC Auto, Powermatic Data, China Sunsine all are somewhat hedgers against inflation in their ways.

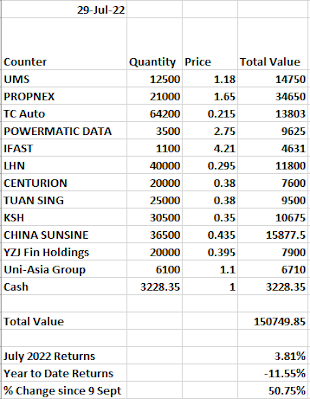

With that, the portfolio now looks like this as iFast is removed (i might come back to this again or take a look at its results time to time and comment on it) but a good analysis on iFast can be found on Kyith's post

In Conclusion, i feel fairly ok with the portfolio although there are a few stocks that are in the portfolio not just because of the immediate results but rather a bit of both immediate and long term thoughts while some are still mid to long thoughts.