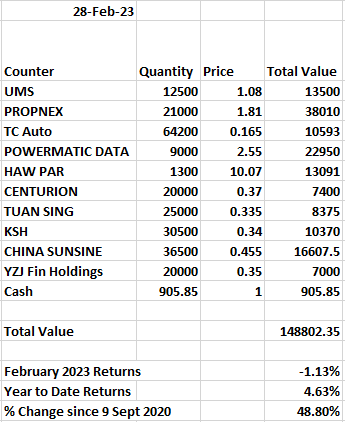

Quick Commentary for the Stocks that released their earnings in February

Propnex - The bottom line does not reflect the true story as there has been impairment of trade receivables being recorded under other expenses offset by derecognition of payables recorded as other income.

Having said that, gross profit is up while revenue has shown an increase in Q4 and Full Year. The increase of 16.88% in 2H 2022 and 7.5% in FY 2022 is much better than APAC Realty's -5% in 2H 2022 and -4.8% in FY 2022. The stock recorded a modest increase on 28 Feb and rightly so as it has proven to be able to increase its revenue despite what many would say is a poorer environment due to interest rates.

TC Auto - As anticipated, the repeated lockdown in 2H 2022 before the 'sudden open up' has resulted in poorer sales in 2H 2022 compared to 1H 2022. Surprisingly, handling and commission fee income actually is higher in 2H 2022 than in 1H 2022. The worst is likely over and 1H 2023 will be crucial.

Haw Par - Lack of Special Dividend might be a turn-off but not that it was anticipated anyway. Despite UOB declaring higher dividends, they will only be credited as dividend income in the upcoming financial result. Perhaps a slight worry is that the growth momentum of its Healthcare Segment has slowed down in 2H, but that is really picking the 1 mark mistake from a boy who got 99/100 for his exam. The ROA of the healthcare business is around 30% in 2022, and is valued at free on the balance sheet.

Centurion - Results not released at point of writing

Tuan Sing - Bells start to ring as the company recorded higher finance expense and reverse into a loss making position in 2H 2022. However, 2023 could finally be the year for Tuan Sing as Gultech seems to be nearing an ipo. It is a company i might want to give a closer look if i can spare some time and effort out.

China Sunsine - Results not released at point of writing

UMS - Have to see if the subcontracting cost come down. The slowdown in growth is anticipated and much will have to depend on if the company is able to get new customers to fill the demand. But given the trend that factories will still be completed, demand looks somewhat healthy.

Conclusion: Most looks rather good actually surprisingly. Those that did not have a much rosier outlook ahead as well apart from UMS which already looks cheap based on current valuations.