To continue the previous trend, if this post goes off, it means i have took a plane and travelled somewhere. This time its Taiwan.

As such, considering the flight price as compared to previous trips is lower, the quality of this post is expected to be not as high.

A company i have added to my shortlist/ waitlist recently is Justin Allen Holdings Ltd (Hkex: 1425). It is a company that is listed in 2019 November and its business entails OEM garment manufacturing of sleepwear and loungewear products. Its major customer is Target and Walmart although the former is 85% of its revenue.

(Company Logo)

Following my trend of looking at the balance sheet first, the company's balance sheet and financials have caught my eye straight away as they look too wonderful to be true.

(Total Equity rising since 2018, Cash has also covered liabilities in 2021 which means i can take a close look at the other parts of the company)

(Revenue and Net income rising in tandem. Looks good as well but is all so good?)

What i like about the company1) Really Good Numbers

There is no sugar coating, the numbers are good and that is that.

The half year numbers pale in comparison to full year number as usually business picks up in 2H of the year. Nevertheless, the past few years have seen an increase in price per product. Yet at the same time, the number of staff at Cambodia has decreased. With its China Plant being unprofitable in 2022, relatively cool to say a huge chunk of profit comes from Cambodia.

(Seasonal Impacts do Occur, 2H usually is better than 1H)

Perhaps a better way to sell koyok will be to present the 1H numbers in comparison but i am slightly lazy so i will just leave it like that.

2) Close to full hiring and expansion plans. Constructing a plant near the delivery location has became a trend recently i have noticed and with 3 factories in the pipeline as well as customers possibly approving new wear products will allow for better revenue in future. In fact, i would say this might mean that it is close to full capacity currently.

From my possibly unreliable sources of the internet, it seems like the Cambodia Factory is close to full capacity as well.

(Company's Expansion Plans)

3)

Major Customer increasing demand over time.(1H and 2H both increased year on year.)

What i dislike about this company1) Balance Sheet can better. Company holds quite a huge sum of financial assets and have seen them being written down in 1H 2022.

For folks who are highly into looking at inventory, trade receivables and various asset ratios, this balance sheet will likely be a mixed bag of results as while receivables has not increased despite an increase of revenue by 30%, payables has increased largely while inventory has also increased by around 40%.

A good gauge will be to refer to the 2021 balance sheet to assess the inventory levels.

Fortunately, the 2021 June levels of inventory look similar to 2022 June. Which means it is not much of a worry. Also with most revenue coming from target, i am not sure how much importance should be place on the receivables.

2)

Highly Volatile Orderbook. As orders are not on a long term contract basis and also subjected to economic demands in US, these are factors that can affect any garment factories in general. There is also a heavy reliance on Target to have not much financial difficulties as well as being able to grow their market share and demand in US.

This is also highlighted in its IPO.

3)

Difficulty in finding more information. While some information on its China Subsidiary which is unprofitable is available, the Cambodia Subsidiary's information is much harder to find and it its not a surprise given that there is probably around 1000 staff there about and the language Cambodia uses (Khmer) is difficult to type / translate around as well.

On the management front, they have been rather low profile or did not win any awards or anything where they would give an interview. The most recent article was about wages in 2022.

Another article was in 2020 which mentioned a change in strategy helping the company.

ConclusionIs this stock a buy currently? Not for myself as i have mentioned a lot of times i do not have excess cash.

How about if i had cash? I would consider because this company has shown good profitability in the past, a potential expansion plans as well as unit price has increased each year while margins have climbed steadily as well. Also, the management themselves hold 67% of the company. I believe that a billion or 2 billion HKD is considered small as Target's apparel sales in 2021 itself is around 140 billion HKD.

Of course there is some concerns over what sizing i should put in(if i had the cash) as a part of me would have liked for the management to explain a bit more on their plans and how they have done well these years while maintaining a lower Cambodia Headcount etc.

In other words, the PR portion can be better communicated. Sometimes even accepting a media/radio interview to share about the company's business and its developments would be decent as well

Although something interesting is that they have paid a 5.9 cents dividend for FY 2021 and there is some reasoning given. 'For the year ended 31 December 2021, the Board proposed a final dividend of HK$0.059 per share,

representing a dividend ratio of approximately 46.6% out of the profit attributable to the owners of the

Company. Given the Group continued to record good results in a challenging environment, the Board

decided to declare dividend at a relatively high dividend ratio to shareholders of the Company for sharing

fruitful returns to them and as an appreciation for their support.'

I would not be surprised if FY2022 results continue to impress.

(Thanks for reading)

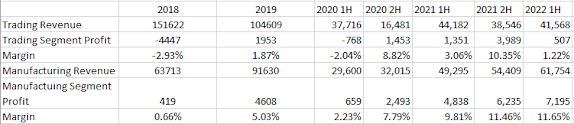

For folks who want to view the half year comparison can refer to the table below.

Anyway if my valuations (which are 99.99% inaccurate) would indicate, i would estimate that 2H 2022 could break 23 million . However, this is depending on what is the maximum capacity they can achieve which is something that they have not said or indicated. From my reading, they do outsource their orders as well so i believe any increase in production should be largely possible.

If productions do hit 23 million in 2H 2022, the profit estimate could look like this.

This means that it is trading at less than 4 PE at the current price of 0.63 (As Full Year EPS will be 0.17)

However at the current price of 0.63, it is trading at book value of 1.64 (above book value) which is a rarity among garment small caps.